Report (PDF)

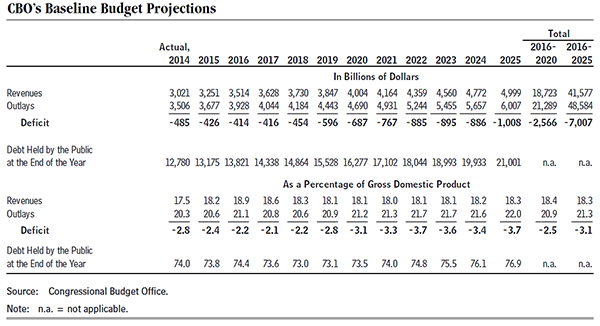

August 25, 2015 - Summary - According to the Congressional Budget Office’s estimates, this year’s deficit will be noticeably smaller than what the agency projected in March, and fiscal year 2015 will mark the sixth consecutive year in which the deficit has declined as a percentage of gross domestic product (GDP) since it peaked in 2009. Over the next 10 years, however, the budget outlook remains much the same as CBO described earlier this year: If current laws generally remain unchanged, within a few years the deficit will begin to rise again relative to GDP, and by 2025, debt held by the public will be higher relative to the size of the economy than it is now.

CBO’s economic forecast, which serves as the basis for its budget projections, anticipates that the economy will expand modestly this year, at a solid pace in calendar years 2016 and 2017, and at a more moderate pace in subsequent years. The pace of growth over the next few years is expected to reduce the quantity of underused resources, or “slack,” in the economy, lowering the unemployment rate and putting upward pressure on compensation as well as on inflation and interest rates.

The Budget Deficit for 2015 Will Be Smaller Than Last Year’s

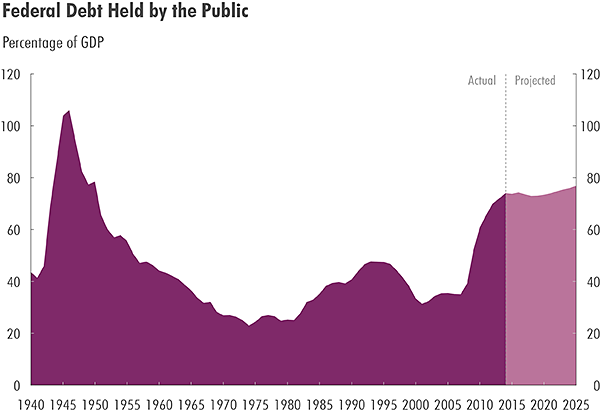

At $426 billion, CBO estimates, the 2015 deficit will be $59 billion less than the deficit last year (which was $485 billion) and $60 billion less than CBO estimated in March (see table below). The expected shortfall for 2015 would constitute the smallest since 2007, and at 2.4 percent of gross domestic product, it would be below the average deficit (relative to the size of the economy) over the past 50 years. Debt held by the public will remain around 74 percent of GDP by the end of 2015, CBO estimates—slightly less than the ratio last year but higher than in any other year since 1950.

Outlays

Federal outlays are projected to rise by 5 percent this year, to $3.7 trillion, or 20.6 percent of GDP. That increase is the net result of a nearly 10 percent jump in mandatory spending, offset by lower net interest payments and discretionary outlays.CBO anticipates that mandatory outlays will be $199 billion higher in 2015 than they were last year. Federal spending for the major health care programs accounts for a little more than half of that increase: Outlays for Medicare (net of premiums and other offsetting receipts), Medicaid, the Children’s Health Insurance Program, and subsidies for health insurance purchased through exchanges and related spending are expected to be $110 billion (12 percent) higher this year than they were in 2014.

In addition, outlays related to the government’s transactions with Fannie Mae and Freddie Mac and for higher education programs will be greater than the amounts recorded last year. Those increases will be partially offset by increased receipts from auctions of licenses to use the electromagnetic spectrum and by reduced spending for unemployment compensation.

Even though federal borrowing continues to rise, CBO expects that the government’s net interest costs will fall by nearly 5 percent this year—mainly because lower inflation this year has reduced the cost of the Treasury’s inflation-protected securities.

CBO anticipates that discretionary spending, which is controlled through annual appropriations, will be about 1 percent less in 2015 than it was in 2014. By the agency’s estimates, defense outlays will drop by more than 2 percent, whereas nondefense discretionary outlays will be only slightly below last year’s amount.

Revenues

Federal revenues are expected to climb by 8 percent in 2015, to $3.3 trillion, or 18.2 percent of GDP. Revenues from all major sources will rise, including individual income taxes (by 10 percent), corporate income taxes (by 8 percent), and payroll taxes (by 4 percent). Revenues from other sources are estimated to increase, on net, by 5 percent. The largest increase in that category derives from fees and fines, mostly as a result of provisions of the Affordable Care Act.Changes From the March Projections

Receipts from individual and corporate income taxes have been greater than anticipated, which largely explains the $60 billion reduction in the projected deficit for 2015; revisions to CBO’s estimates of outlays had almost no net effect.Rising Deficits After 2018 Are Projected to Gradually Boost Debt Relative to GDP

In CBO’s baseline projections, the budget shortfall declines to $414 billion next year but then rises substantially, to $1.0 trillion in 2025. By those estimates, which incorporate the assumption that current laws will generally remain the same, the combination of significant growth in spending on health care and retirement programs and rising interest payments on federal debt would outpace growth in revenues.The outlook for the 10-year projection period does not differ substantially from the one CBO described in March. As in the previous projections, deficits as a percentage of GDP are estimated to remain below this year’s level for the next three years but then begin to rise. In CBO’s current baseline, the deficit falls to 2.1 percent of GDP in 2017, but in the latter half of the decade, deficits average 3.5 percent of GDP. The cumulative deficit between 2016 and 2025 is $7.0 trillion.

Such deficits would push debt held by the public up to 77 percent by the end of the 10-year projection period, roughly twice the average it has been over the past five decades (see figure below). Beyond 2025, if current laws remained in place, the same pressures that contribute to rising deficits during the baseline period would accelerate and push debt up sharply relative to GDP.

Such high and rising debt would have serious negative consequences for the nation:

- When interest rates returned to more typical, higher levels, federal spending on interest payments would increase substantially.

- Because federal borrowing reduces national saving over time, the nation’s capital stock would ultimately be smaller, and productivity and total wages would be lower than they would be if the debt was smaller.

- Lawmakers would have less flexibility than otherwise to use tax and spending policies to respond to unexpected challenges.

- Continued growth in the debt might lead investors to doubt the government’s willingness or ability to pay its obligations, which would require the government to pay much higher interest rates on its borrowing.

Outlays

In CBO’s projections, federal outlays remain near 21 percent of GDP for the next several years. Later in the coming decade, under current law, growth in outlays would outstrip growth in the economy; outlays would rise to 22 percent of GDP in 2022 and remain at that level through 2025. (Over the past 50 years, outlays have averaged about 20 percent of GDP.) That trend reflects significant growth in mandatory spending—particularly in federal spending for health care, Social Security, and interest payments—offset somewhat by a decline (relative to the size of the economy) in spending subject to annual appropriations.Outlays for mandatory programs are projected to rise from their current level of near 13 percent of GDP to 14 percent by the latter part of the projection period. That increase is mainly attributable to significant growth in spending on health care and retirement programs— caused by the aging of the population and rising per capita health care costs. In CBO’s baseline, between 2015 and 2025, federal outlays for the government’s major health care programs, measured as a share of GDP, rise by 1 percentage point, whereas outlays for Social Security grow by 0.7 percentage points. All other mandatory spending falls relative to the size of the economy.

The government’s interest payments on debt held by the public are projected to rise sharply over the next 10 years because of two factors: rising interest rates and growing federal debt. Because interest rates are now very low by historical standards, net outlays for interest are similar to amounts recorded 15 to 20 years ago, when federal debt was much smaller. As those rates rise, and as debt continues to mount, the government’s cost of financing that debt will climb.

By contrast, discretionary spending is projected to drop from 6.5 percent of GDP this year to 5.1 percent in 2025. That projection incorporates the assumption that the caps on budget authority originally set by the Budget Control Act of 2011, as subsequently reduced, will stay in place through 2021.

Revenues

Revenues are projected to rise to almost 19 percent of GDP in 2016, primarily because several provisions of law expired at the end of calendar year 2014. Under provisions of current law, revenues would recede to roughly this year’s percentage of GDP by 2019, CBO estimates. That drop stems mostly from an expectation that corporate profits as a share of GDP will decline in the coming years in the wake of rising costs of labor and interest payments on businesses’ debt. In addition, in CBO’s projections, remittances to the Treasury from the Federal Reserve—which have been unusually high since 2010—return to more typical levels. Those factors are only partially offset by the continued increase (relative to GDP) of receipts from individual income taxes. That increase causes CBO’s projections of overall receipts to rise slowly in relation to GDP after 2021, though they still remain close to 18 percent of GDP through 2025.Changes From CBO’s Previous Budget Projections

CBO’s current baseline projections of the deficit for the coming decade are somewhat smaller than the amounts the agency estimated in March 2015. Over the 2016–2025 period, the cumulative deficit is about $200 billion lower, the net result of estimates for outlays and revenues that are lower by $372 billion and $170 billion, respectively.Most of the reduction on the outlay side of the budget ledger stems from lower net interest costs, which occur because CBO’s forecast for interest rates is now lower than it was before. Estimates of spending for some mandatory programs are also lower as a result of smaller projected cost-of-living adjustments. Those reductions in spending are partly offset by the estimated increase in outlays resulting from the Medicare Access and CHIP Reauthorization Act of 2015 and various other revisions to the projections.

Technical adjustments account for the largest changes to CBO’s revenue projections, reducing them by $236 billion through 2025 from the amounts estimated in March. Higher-than-expected tax collections in recent months caused CBO to increase its revenue projections for the next two years, but other factors, including new information from tax returns, caused the agency to reduce its projections for the later years of the 10-year period. The effects of those technical changes were partially offset by the revised economic outlook, including a slightly higher projection for wages and salaries and a slightly lower projection for interest rates.

The Economy Is Expected to Grow Modestly This Year and at a Solid Pace for the Next Few Years

Although real (inflation-adjusted) GDP grew weakly early in 2015, recent data indicate that the economy is now on firmer ground, and CBO expects the pace of economic activity to pick up in the second half of this calendar year and over the next few years. After that, the agency anticipates moderate economic growth, constrained by relatively slow growth in the labor force.The Economic Outlook for 2015 Through 2019

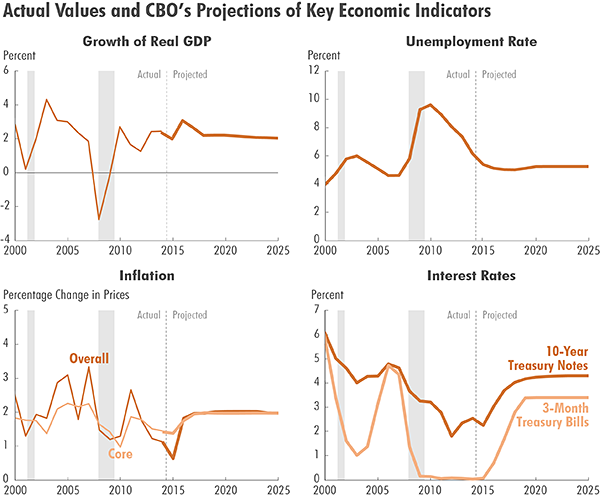

Under the assumption that current laws governing federal taxes and spending will generally remain in place, the agency projects that real GDP will grow by 2.0 percent this calendar year, by 3.1 percent in 2016, and by 2.7 percent in 2017, as measured by the change from the fourth quarter of the previous year (see figure below). For 2018 and 2019, the agency projects that the economy will grow at an average annual rate of 2.2 percent. In CBO’s estimation, the economic expansion through 2019 will be driven primarily by increases in consumer spending, business investment, and residential investment.

With that faster pace of growth in output, slack in the labor market—which is indicated by such factors as an elevated unemployment rate and a relatively low rate of participation in the labor force—is expected to dissipate over the next few years. According to CBO’s projections, the unemployment rate will fall from 5.2 percent in the fourth quarter of 2015 to 5.0 percent in the fourth quarter of 2017. As slack in the labor market diminishes and firms must increasingly compete for a shrinking pool of unemployed or underemployed workers, growth in hourly compensation is expected to pick up. The upward pressure on compensation will encourage some people to enter or stay in the labor force, in CBO’s estimation. That development will slow the longer-term decline in labor force participation, which is the result of both underlying demographic trends and federal policies, but it will also slow the fall of the unemployment rate.

Over the next few years, reduced slack in the economy will put upward pressure on inflation and interest rates. Nevertheless, CBO expects the rate of inflation (as measured by the price index for personal consumption expenditures [PCE]) to stay below the Federal Reserve’s goal of 2 percent through mid-2017—an outcome that is consistent with some remaining but diminishing slack in the economy and with widely held expectations for low and stable inflation. CBO anticipates that the interest rate on 3-month Treasury bills, which has been near zero since the end of 2009, will begin increasing in the second half of 2015 and rise to 3.4 percent by the end of 2019. The rate on 10-year Treasury notes, CBO expects, will rise from an average of 2.4 percent in the second half of 2015 to 4.2 percent by the end of 2019.

The Economic Outlook for 2020 Through 2025

CBO’s projections for the latter half of the coming decade are not based on forecasts of cyclical developments in the economy, but rather on projections of underlying trends of indicators such as growth in the labor force, the number of hours worked, and productivity. By those projections, both actual output of the economy and potential (maximum sustainable) output will expand at an annual average rate of 2.1 percent, faster than the estimated 1.5 percent average annual growth in potential GDP during the current business cycle so far (that is, between 2008 and 2014). The projected pace is slower than it was in the 1980s, 1990s, and early 2000s, though, primarily because the labor force is expected to grow more slowly than it did then. Real GDP is projected to be about one-half of one percent below real potential GDP from 2020 through 2025, reflecting the historical average over the several business cycles between 1961 and 2009.Corresponding to that projected gap between output and potential output, in CBO’s projections the unemployment rate over the 2020–2025 period—at 51⁄4 percent—remains slightly above the natural rate (the rate arising from all sources except fluctuations in the overall demand for goods and services). Inflation (as measured by the PCE price index) is expected to average 2.0 percent per year, and interest rates for 3-month Treasury bills and 10-year Treasury notes are projected to average 3.3 percent and 4.3 percent, respectively. Those rates would be well above current rates but below average rates over the 25 years before the most recent recession. Compared with those historical levels, projected interest rates will be dampened by lower inflation as well as by slower growth in the labor force and slightly slower growth of productivity.

Changes From CBO’s Previous Economic Projections

CBO’s current economic projections differ in certain respects from those the agency released in January 2015. CBO now projects slower growth of real GDP this year and slightly faster growth between 2016 through 2019 than it did in those previous projections. In addition, unemployment rates and long-term interest rates are lower over the 2015–2025 period in CBO’s current projections than they were in January’s. Inflation is now estimated to be lower this year and next year than was previously expected.Source: CBO