Marketplace Enrollment Could Fall to About 17.5 Million in 2026

May 19, 2026 - The average Affordable Care Act (ACA) Marketplace deductible experienced the steepest increase in history—growing by 37% or over $1,000, from $2,759 in 2025 to $3,786 in 2026 as enhanced premium tax credits expired, according to a new KFF analysis.

After the enhanced tax credits ended, many Marketplace shoppers shifted toward lower-premium, higher-deductible plans. Between 2025 and 2026, sign-ups for bronze plans jumped from 30% to 40% of total plan selections—growing from 7.3 million to 9.2 million people.

Meanwhile, sign-ups for silver Marketplace plans, which have higher premiums and lower cost-sharing, hit the lowest levels in the program’s history. Silver plan sign-ups fell from 57% to a record-low 43%, dropping from 13.7 million to 9.8 million people. The share of Marketplace enrollees who signed up for cost-sharing reduction (CSR) silver plans—which reduce out-of-pocket costs for deductibles, copayments, and coinsurance for lower income enrollees—also fell to the lowest level on record: 37%.

While higher deductible plans have lower premiums, they also result in bigger out-of-pocket bills for patients, straining household budgets and leading to potential medical debt and poorer access to care. Most Marketplace enrollees (67%) said they would likely cut spending on basic household needs if their annual health costs increased by $1,000, according to a KFF survey conducted last November, before the enhanced credits expired.

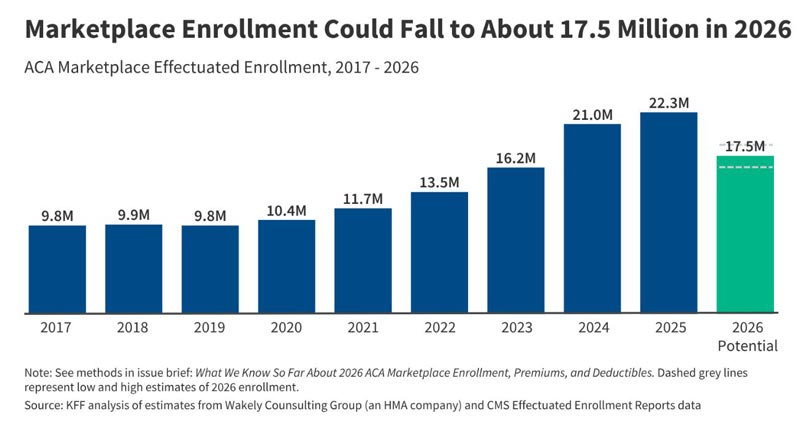

How Much Marketplace Enrollment Could Fall

Marketplace enrollment could ultimately decline by 21.5% or nearly five million people this year, falling from 22.3 million people in 2025 to about 17.5 million in 2026, according to KFF analysis of estimates from Wakely Consulting Group on premium payments as well as federal data.

About 23 million people signed up for Marketplace plans during the 2026 Open Enrollment Period—over a million fewer than in 2025 and the sharpest single-year drop in raw numbers since the ACA Marketplaces launched—and more enrollment declines are likely this year due to higher out-of-pocket premiums with the enhanced tax credits expired.

A significant number of Marketplace enrollees are expected to lose their coverage mid-year because they fail to make premium payments, which have increased by an average of 58% from $113 to $178. Accounting for this drop from unpaid premiums as well as mid-year attrition and other factors, Wakely estimates that average effectuated enrollment in the individual market could decline by 17% to 26% between 2025 and 2026.

Who Dropped Marketplace Coverage and Where

Middle-income individuals represent a disproportionately larger share of those who dropped ACA Marketplace coverage during the 2026 Open Enrollment Period. When the ACA’s enhanced subsidies expired, the “subsidy cliff” reemerged, causing many middle-income people to drop their coverage because they earned too much to qualify for standard subsidies but too little to afford unsubsidized premiums.

People with incomes over this subsidy cliff (400% or more of the federal poverty level, or $62,600 for a single person in 2026) made up just 7% of 2025 Marketplace enrollment but nearly half (48%) of the decline in plan selections from 2025 to 2026.

Most states experienced major drops in ACA sign-ups. Marketplace sign-ups fell in 41 states, with the largest drops seen in North Carolina (22%), Ohio (20%), West Virginia (17%), and Indiana, Delaware, and Arizona (all 16%). Many of these states saw rapid Marketplace enrollment growth under the enhanced subsidies, suggesting that higher out-of-pocket premium contributions following their expiration may have led some Marketplace enrollees to drop their coverage.

State-based exchanges, many of which have their own supplemental premium subsidy programs and more robust outreach efforts, tended to retain higher shares of enrollees than states with federally facilitated exchanges.

Source: KFF